“Economics is about making choices in the presence of scarcity.”

Why study Economics?

Need and Want

A Need is something that a person must have in order to thrive(Necessity), a decent source of income(a job).

A Want is a choice(desire to become an IAS officer). A desire, which a person may or may not be able to get. Life goes on if a person doesn’t get what they want.

Example: We need to eat in order to live. But the choice of what to eat leans toward want.

Each person has his or her own list of wants, each with a varying level of importance. Furthermore, wants can change over a period of time. This is in contrast to needs, which remain constant throughout the lifetime of the person.

“Our wants are unlimited but the resources are scarce.”

“The first lesson of economics is scarcity: there is never enough of anything to fully satisfy all those who want it”.

Fundamentally, without scarcity, there would be no need for economics because we would have an infinite supply of anything we could imagine available immediately for no cost or trade off.

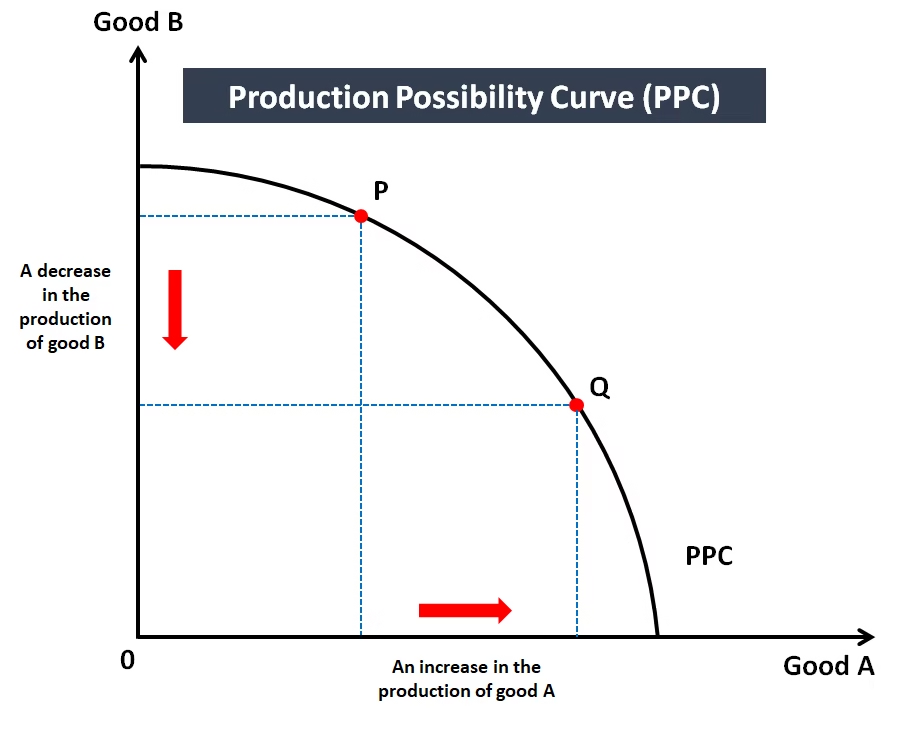

To get one thing, we usually have to give up something else. Making decisions requires trading one goal for another(pursuing the dream of becoming an IAS officer or a film actor).

Example: Allocating Resources to produce Guns or Grains, Equality Vs Efficiency, Environment Vs Faster Growth, IAS Officer or Film Actor.

“The Cost of Something is What You Give Up to Get It”.

Opprotunity cost is the cost of next best alternative.

Because people face trade off, making decisions requires comparing the costs and benefits of alternative courses of action.

Opportunity cost is whatever must be given up in order to obtain some item or next best alternative forgone.

Example: The opportunity cost of preparing civil services is the money you could have earned if you used that time to work.

“Similarly the money the government spends(taxpayers money) on freebies is the money it can’t afford to spend on infrastructure”.

Many people hear the word economics and think it is all about money, economics is not just about money. It is about weighing different choices or alternatives. Some of those important choices involve money, but most do not. Most of your daily, monthly, or life choices have nothing to do with money, yet they are still the subject of economics.

“ Studying economics might not make you rich, but it definitely helps you understand why you are poor ”.

It is that discipline of study which is concerned with the production, consumption, and transfer of wealth.

Economics, at its core, is the study of how best to use those limited resources. In basic terms, economics is an academic attempt to put the world’s limited resources to their best use.

Difference between Economics and Economy

The relation between economics and the economy, is that of theory and practice. While the former is a discipline studying economic behaviour of human beings, the latter is a still frame picture of it.

Economy is economics at play in a certain region. This region is best defined today as a country, a nation – the French Economy, the Russian Economy, etc. economy as such means nothing. It gets meaning once it is preceded by the name of a country, a region, block, etc.

Economic Activity

An economic activity is an activity of providing, making, buying, or selling of commodities or services by people to satisfy their day-to-day needs of life. Economic activities include any activity that deals with the manufacturing, distributing, or utilising of products or services.

“Any activity that has a value and price attached”

Example: Business, Job

Non-Economic Activity

A non-economic activity is an activity performed with the purpose of rendering services to others without any considerations of financial gains. Activities that are initiated for personal content or for meeting human sentiments are non-economic activities.

“Any activity that has a value and no price attached”

Example: Free time activities, Social welfare activities.

The two main branches of Economics

- Micro Economics

- Macro Economics

Microeconomics, is the study of economics at an individual, group or company level, it explores issues such as how families reach decisions about what to buy and how much to save.

- Microeconomics explains the inter –relationships between economic units like consumers, commodities, firms, industries, markets, etc.

- Microeconomic theory describes product pricing which explains the theories of demand, production, and factor pricing which explains concepts of wages, rent, interest, and profit.

- Understanding microeconomics helps a great deal on individual decision making i.e., managerial decision making.

Macroeconomics, on the other hand, is the study of a national economy as a whole. Macroeconomists study aggregated indicators such as GDP, unemployment rates, national income, price indices, and the interrelations among the different sectors of the economy to better understand how the whole economic functions..

- Macroeconomics analyses the fluctuations and trends in the overall economic activity in a country and/or between various countries in the world.

- Macroeconomic theory describes the theory of income and employment to explain economy – wide consumption and investment, the theory of economic growth, and the macro theory of distribution.

- Macroeconomic study is vital in the formulation and execution of economic policies by government.

- Macroeconomic analysis includes study of national aggregates of output, income, expenditure, savings and investment.